Over a two-year period, a $35M+ ARR Instructure product was transformed into an AI-native solution and deployed at scale for more than 2 million users worldwide — introducing explainable and compliant AI into the learning ecosystem without compromising trust, accessibility, or operational stability.

App-Web Design

Depot

I was focusing on revamping Depot's comprehensive CI/CD developer experience, covering everything from pipeline creation and secrets management to diagnostics, logs, artifacts, and governance. The goal was to minimize friction in essential processes, simplify intricate steps, and provide an accessible, scalable design system that could grow with the product.

App-Web Design

Raiffeisen

Over 2 years the full mobile banking ecosystem was rebuilt and deployed across 16 countries, resulting in a +670% increase in app downloads and more than €300M in additional annual digital transaction volume — driven by restored trust, a new design system, and a redesigned end-to-end experience.

App-Web Design

Bitpanda

Bitpanda is the trading platform that Raiffeisen Bank customers use when they buy and sell digital assets through the bank’s app. During the 2 redesign I worked on both the direct Bitpanda product and the bank ready variant used inside Raiffeisen. The same system that later contributed to 53% user growth (3.4M → 5.2M) and more than €140M+ annual digital revenue across the period.

App-Web Design

Benker

Benker is a digital banking platform built on blockchain and tailored for secure, multi currency account management across Europe. As design lead and hands on designer, I redefined onboarding and transaction flows, which increased digital transaction volume by 150%, improved KYC success rates by 30%, and reduced time to first successful transaction by 50%.

App-Web Design

OnRobot

Built a tablet-first HMI in 12 weeks to eliminate teach-pendant scripting and spreadsheet math. In pilots it cut first-time setup by 42%, reduced input errors by 63%, slashed training time by 75%, and drove a +36 NPS among operators.

App-Web Design

SportsGambit

SportsGambit is a decentralized prediction market leveraging advanced AI to give you an edge. The platform's core feature is the ability where a user can build, train, and deploy custom prediction agents. These autonomous agents continuously learn and improve, analyzing specific sports or events to deliver a curated feed of high-probability outcomes directly to your dashboard. This eliminates manual research and allows for swift, one-tap wagering, combining AI-driven insights with the security and transparency of the blockchain.

My Role & Mission

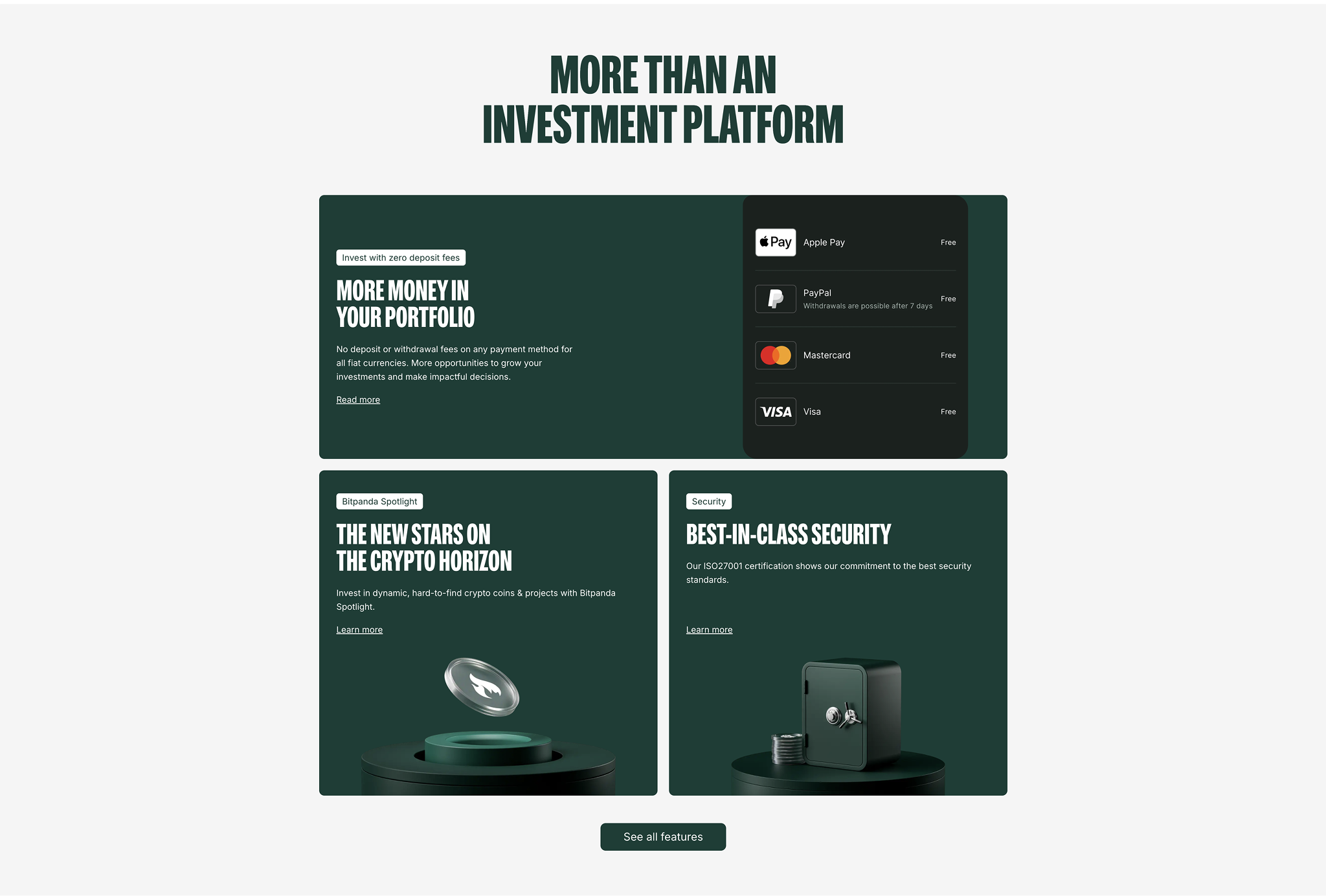

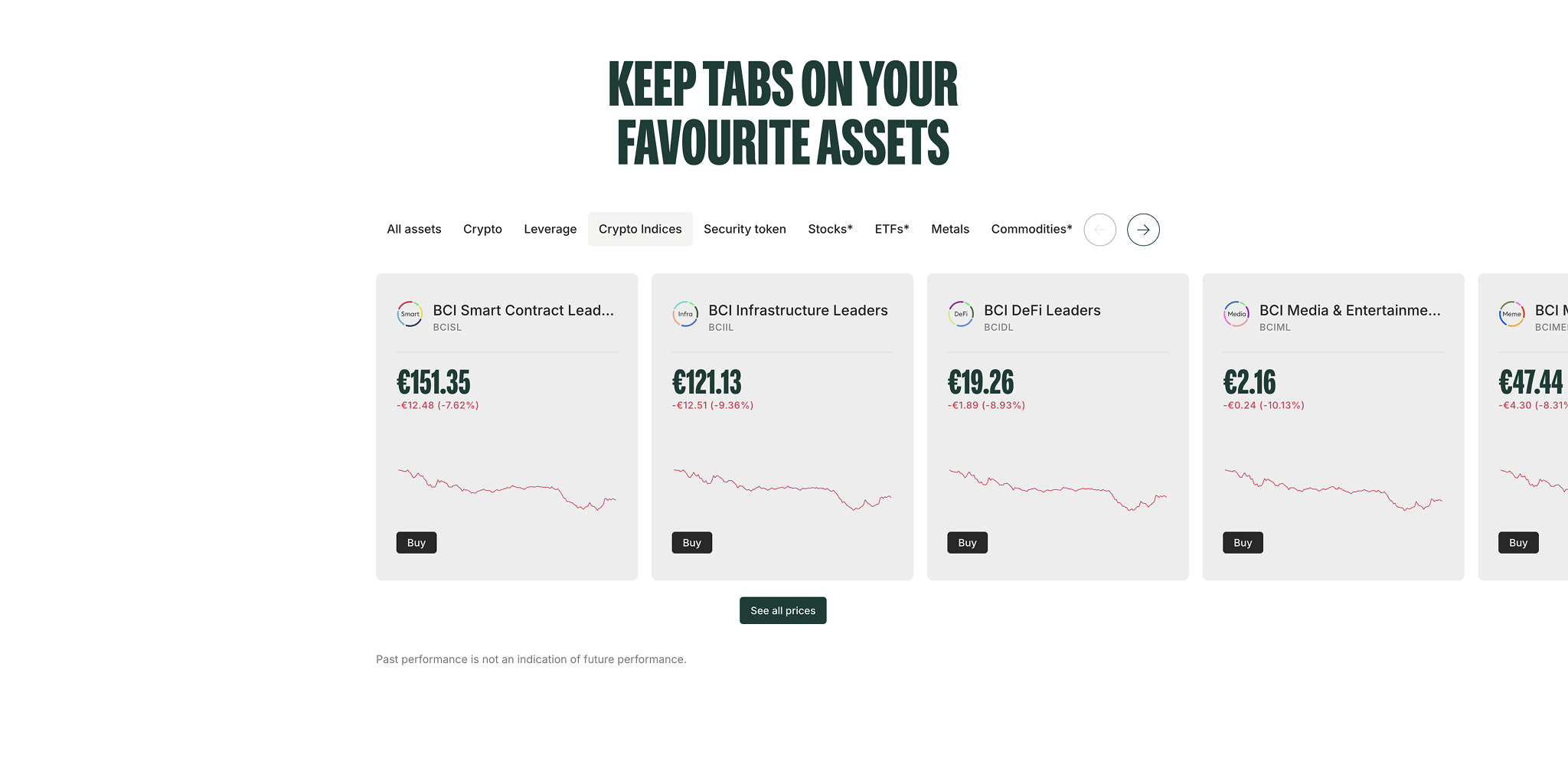

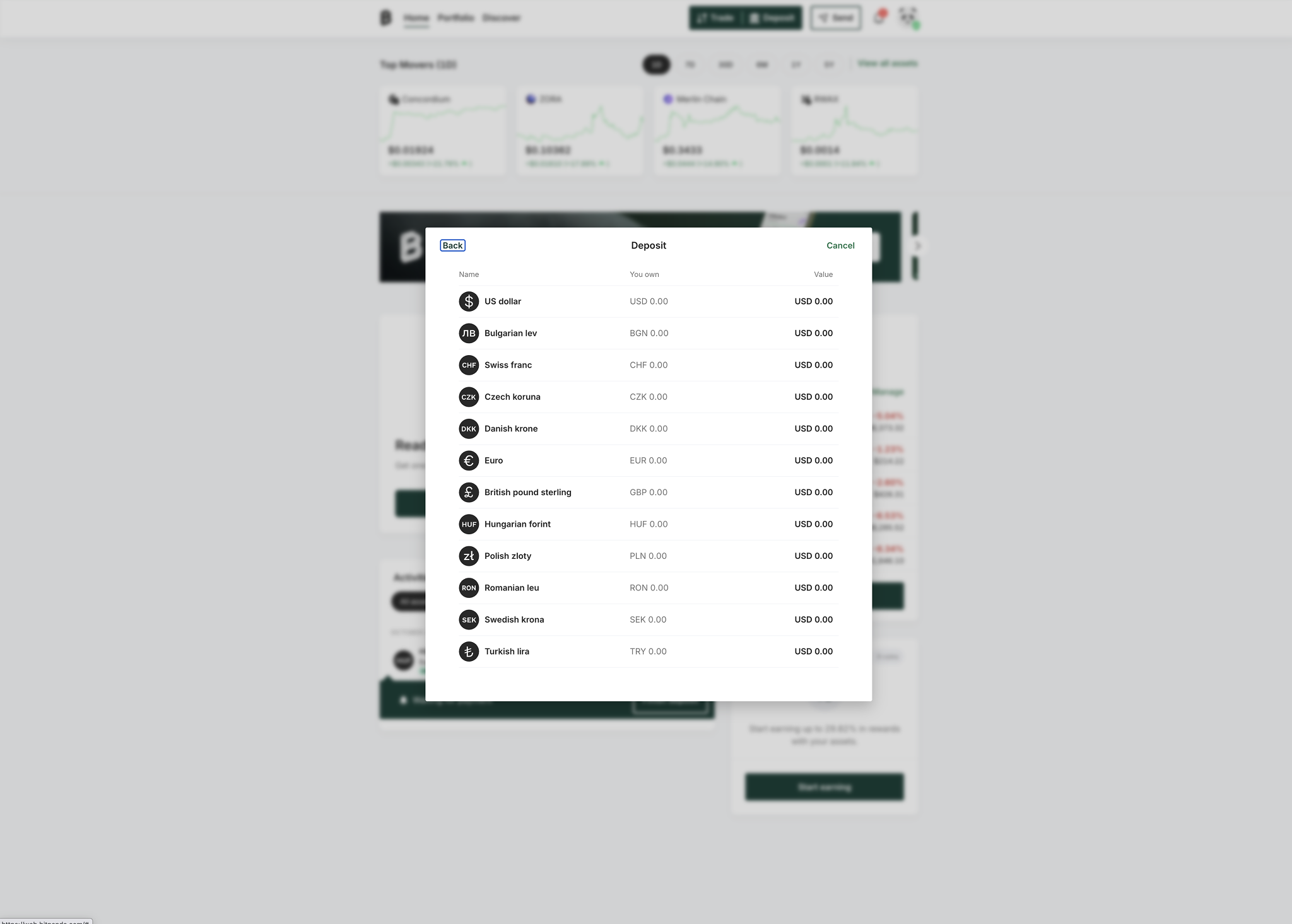

Led the redesign of Bitpanda’s core trading and portfolio experience used by millions of retail users, plus the bank-ready variant later adopted by Raiffeisen via white-label distribution. Scope included the end-to-end deposit journey (KYC + card validation) to meet banking-grade compliance while staying fast for everyday users. Objective: keep Bitpanda’s speed and clarity while making it credible and adaptable for regulated environments. Norbert Barna

Challenges

Bitpanda scaled quickly, but legacy flows weren’t designed for bank-grade scrutiny or lower-confidence users arriving through institutional channels. High-risk actions (deposit, trade execution, withdrawal) needed stronger confirmations and trust cues. Portfolio understanding was low, risk states were inconsistent, and distribution partners (e.g., Raiffeisen) required better accessibility, localization, and auditability—without forking the product. Norbert Barna

The Process

Rebuilt the full financial journey—onboarding → deposit (KYC/card) → discovery → execution → portfolio → history—around trust, reversibility, and clarity. Standardized risk/state communication, redesigned confirmations for credibility and cognitive safety, and introduced a consistent visual + verbal system so the product became bank-ready without extra friction. Compliance and Raiffeisen legal/ops partnered on tone and localization; changes were user-tested to raise understanding and confidence before broad rollout. Norbert Barna

Who We Designed For

Retail traders who need clear, low-friction deposit and first-trade flows

New, low-confidence users entering via bank distribution who need extra guidance and trust

Compliance/legal partners who require auditability, accessibility, and localization across markets Norbert Barna

UX Methods & Why They Were Used

Contextual inquiry & task shadowing: saw how users actually fund accounts, place first trades, and review portfolios—revealed where trust breaks.

JTBD & task mapping: focused on outcomes like fund successfully, place first trade, understand positions & risk, withdraw safely.

Trust first, then speed: visible guardrails and reversible actions without adding drag.

State clarity everywhere: explicit empty/error/loading/latency/risk states.

One pattern, many markets: reusable components so bank and retail users share a consistent mental model.

Explainability over mystery: confirmations that summarize what’s happening, why it’s safe, and what to do next.

Governance & Rollout

Compliance/legal co-review with Raiffeisen to align tone, localization, and audit expectations.

Feature-flagged cohort ramps with rollback plans to avoid disruption during high-traffic windows.

Live dashboards for conversion and error monitoring across onboarding, deposit, and execution.

What Was Shipped

Redesigned deposit journey (KYC + card validation) with bank-grade confirmations

Standardized risk/state design and trust cues across critical flows

Consistent visual + verbal system to make the product bank-ready without forking

Reusable components enabling faster multi-market rollout and white-label distribution (incl. Raiffeisen) Norbert Barna

Outcome (2021–2022)

User base: ~3.4M → 5.2M (+53%)

Digital revenue: ~€90M → €140M+ (≈ +55%)

Time to first successful trade:~40% faster (activation uplift)

Distribution: white-label readiness unlocked bank distribution (incl. Raiffeisen) without a separate codebase

Speed of expansion:~30% faster time-to-new-market via component/system reuse

Behind the Decisions: Reflections & Trade-offs

Bitpanda sat between two very different worlds: retail crypto speed and traditional banking trust. Either side on its own is easy. The hard part is building one system that works for both.

We could have forked the product: one flow for “degenerate speed,” another for “bank clients.” Short-term, that would have been simpler. Long-term, it would have been a maintenance nightmare. Instead, we chose the harder path: define one shared mental model for money movement and bake it into confirmations, states, and risk cues that retail users understand and banks can sign off on.

That decision is the reason the same design work later powered Raiffeisen’s white-labeled app without a rewrite. We traded a few flashy crypto micro-patterns for boring but essential things: consistency, explainability, and localizable language that regulators and first-time investors can both live with.